William Lipovsky

William Lipovsky

Writing a check payable to cash is as simple as writing “cash” on the “pay to the order of” line.

However, checks written to cash are risky because anyone can cash them. Some banks may refuse to cash a check written for cash or put a hold on it to prevent fraud.

Below, we have the step-by-step instructions for how to write a check payable to cash, plus the list of safer alternatives.

What Is a Check Payable to Cash?

A check payable to cash is exactly as it sounds: a check that has been made payable to “cash,” rather than to a recipient’s name.

Checks written for cash offer an alternate way to withdraw cash from your account or to transfer funds between accounts.

For example, if you want to move $50 from your checking to your savings account, you can write a check to cash to withdraw the $50 from your checking account. You can then deposit the cash at your bank or an ATM.

Making a check payable to cash is also an option if you don’t know the full or exact name of the payee; he or she can still deposit the check this way.

Risks of Writing Checks for Cash

Checks written for cash are convenient, but because there is no name on the “pay to the order of” line, they’re also risky. Once you write a check for cash, anyone can cash it.

Once you’ve written this type of check, you should treat it like cash, and make sure you keep track of it.

Some banks refuse to honor checks written for cash because of the risk of fraud. Your bank may choose not to cash the check, or it may put a hold on your funds until you can verify that the check is being used properly.

However, if you go to a bank at which you have an account and you’re a customer in good standing, the bank will likely cash your check for you.

Additionally, since checks to cash don’t tell you who the money is for, keeping financial records of them can be tricky. Finding out the exact name of the payee and making the check out to them may end up being the simpler option.

How to Write a Check Payable to Cash

Writing a check payable to cash is similar to writing an ordinary check. First, begin filling out the check the way you normally would; instead of writing a name or company on the pay-to-order line, simply write “cash.”

Next, write out the value of the amount of cash you need, as you would on a normal check.

Once you sign the check, it will be valid to cash.

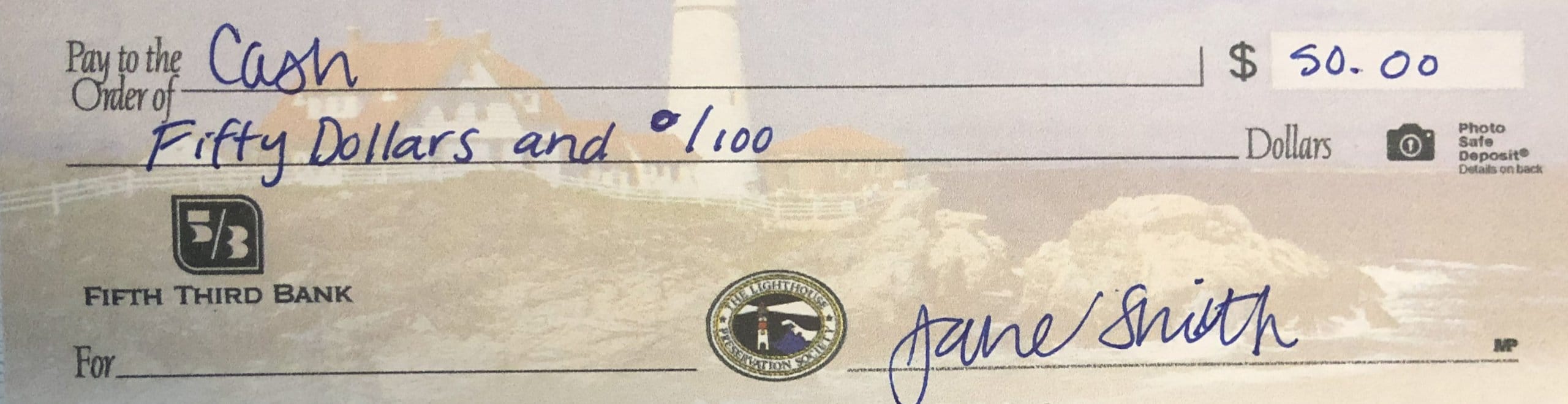

We provide an example written for $50 cash by “Jane Smith” below.

How to Cash and Deposit a Check for Cash

If you’ve received a check written to cash, you can deposit it the same way you would any other check.

Your best bet is to visit the bank that issued the check — this bank may be more willing to cash the check since it was written by an account holder.

Other banks may refuse to honor checks for cash in an attempt to prevent fraud. Also, if the cash amount is very large, the bank may not give you the full amount in one transaction, for security reasons.

The bank may also place an extra hold on the check to make sure it’s legitimate.[1]

To avoid these extra wait times or being turned away by your teller, you can request that all checks you receive are made payable to you by name.

For a list of places that cash checks, see our article listing more than 30 places that cash checks.

What If You Misplace a Check Written to Cash?

If you lose a check made payable to cash, anyone who finds it can cash it. Without a recipient’s name, a bank or store that agrees to cash the check will assume that the person in possession of the check is the correct recipient.

If you lose a check written to cash, you should contact your bank to stop payment of the check immediately. As long as no one has already cashed the check, stopping the payment will prevent the funds from being withdrawn from your account.

You can request a stop payment of your check online, over the phone, or in person with a teller.

If you’re unable to stop payment and someone other than the intended payee uses the check, you may have to take legal action to get the money back or may simply lose the cash. Our related research has more about what to do if your check is stolen or cashed.

Alternatives to Writing Checks for Cash

Writing a check for cash is a fast and straightforward process, but there are ways to transfer money that are just as easy and far less risky.

Below, we list the safer alternatives to writing checks payable to cash.

For Transfers

- Online banking: Your bank’s website or mobile app should offer options for account-to-account and bank-to-bank transfers.

- Teller transfer: Visit a teller in your bank’s lobby. Brick-and-mortar banks often provide the same type of transfer services available online.

- Third-party services: Services like PayPal, Google Pay, or the Cash App offer more ways to transfer money. On PayPal, for example, you can transfer money in and out of your bank account, as well as to other PayPal accounts. These services take some additional time and effort to register for, but once your accounts are set up, they are as efficient as other types of transfer. Some other examples of online money-transfer programs include WePay, Skrill, ProPay, Dwolla, Braintree, Stripe, and Payoneer.

- Write a check to yourself: Instead of another person’s name, simply write your own name on the “pay to the order of” line. You can then deposit the check into a different account. You may need to provide photo identification when cashing a check written to yourself.

Note: Banks, digital wallets, and other financial services often set limits on how much money you can transfer in a single transaction, a day, or a month. Be aware of your account’s rules before scheduling any transfers.

For Unknown Payees

There are no direct alternatives to writing a check made payable to cash if you’re writing the check to someone else.

Traditional check alternatives like money orders and wire transfers are more secure than checks made payable to cash, but they also require you to know the payee’s full name and other personal information.

If you’re able, it’s best to ask for the recipient’s full name and write the check directly to the recipient.

For Withdrawals

- ATMs: You can use the ATM at your own bank or find an ATM at another bank or nearby store. ATMs are easy to find and allow you to withdraw money from your checking account. Be aware that fees may apply if you use an ATM outside of your bank’s network.

- Cash back: Many retailers, especially grocery stores, allow customers to get cash back at the register. Some stores allow you to withdraw as little as $5, and others will enable you to withdraw over $100 in a single transaction. For more details on getting cash back at stores, see our dedicated articles on gas stations that do cash back, stores that give $5 and $10 cash back, and the stores that give the most cash back.

- Write a check to yourself: Write your own name on the pay-to-order line. You’ll be able to cash the check and get the money you wish to withdraw. Be aware of any check cashing fees and ID requirements at the place where you plan to cash your check.